HDB Owners: Your Buyer Pool May Be Shrinking Before You Realise It

- Vann Lim

- 11 hours ago

- 6 min read

For many Singaporeans, a fully paid HDB flat represents security.

There is no outstanding mortgage. The renovation is already done. The neighbourhood is familiar. The MRT, market and coffee shop are nearby. Perhaps the children even grew up in the home.

So naturally, the question becomes:

“The flat is fully paid. Why should I sell?”

It is a perfectly reasonable question.

In fact, selling simply because your flat is getting older would be the wrong way to think about it. A home is not just an investment. It provides stability, convenience and emotional value that cannot always be measured in dollars.

But there is another question that HDB owners should consider:

Even if your flat remains valuable, will it remain easy for the next buyer to purchase?

That distinction matters.

Subscribe to our newsletter if you enjoy insights like this.

A Valuable HDB Flat Is Not Always a Liquid One

As an investor, I have learnt that value and liquidity are two different things.

Your HDB flat may still have a good location, a spacious layout and a beautiful renovation. However, if fewer buyers can comfortably finance it, your potential buyer pool gradually becomes smaller.

The flat does not suddenly become undesirable.

Instead, the change usually happens slowly:

Some younger buyers may find the remaining lease unsuitable for their long-term plans.

Some may face limits on how much CPF they can use.

Others may qualify for a lower loan amount and need to contribute more cash.

Families may compare the flat against newer resale options with longer leases.

Each factor removes a small number of potential buyers.

Individually, this may not appear significant. Collectively, it can affect demand, the time needed to secure an offer and the eventual price a buyer is prepared to pay.

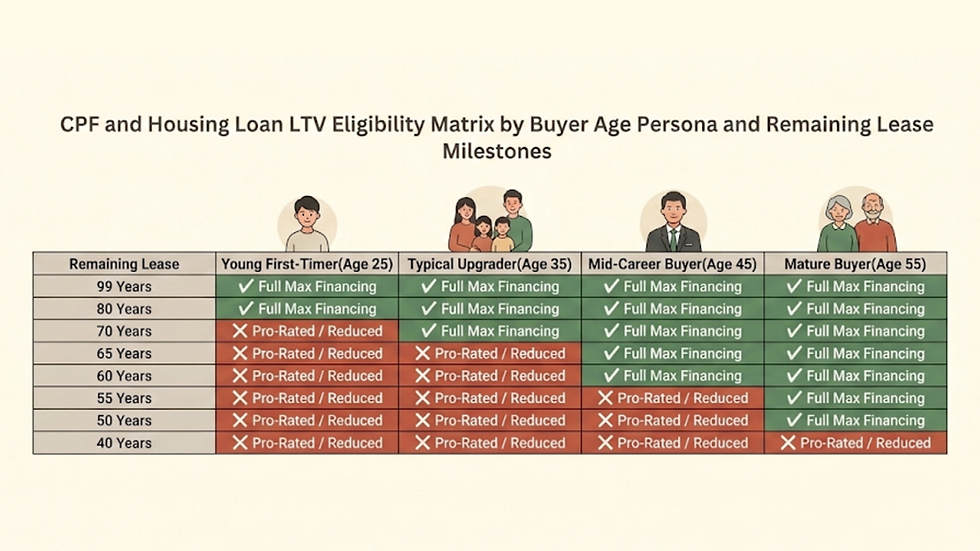

Why the Remaining Lease Affects Your Future Buyer

When someone purchases an HDB flat, they are not evaluating only the location and condition of the home.

They must also consider whether the remaining lease works for their age, financing and future housing plans.

Under current CPF rules, a property’s remaining lease should cover the youngest buyer using CPF until age 95 for the buyers to enjoy the full applicable CPF housing usage limit. Where the lease does not cover the youngest buyer until age 95, the amount of CPF Ordinary Account savings that can be used may be pro-rated.

The same age-95 consideration applies to an HDB housing loan. The maximum HDB loan-to-value limit is currently 75% when the remaining lease covers the youngest applicant until age 95. Otherwise, the loan limit may be prorated.

This does not mean an older flat cannot be sold.

It means the profile of the ideal buyer may change.

A young couple who depend heavily on CPF and financing may hesitate. An older buyer, a cash-rich buyer or someone purchasing primarily for the location may still find the flat suitable.

The issue is not that there will be no buyers.

The issue is whether there will be enough suitable buyers competing for your flat when you eventually decide to sell.

Your Buyer Pool Determines Your Exit

Imagine that a couple in their 30s views your flat.

They love the layout. The bedrooms are spacious. The MRT is nearby, and the home is within their preferred school zone.

But after working through the numbers, they realise that the remaining lease affects the amount of CPF or financing available to them.

They may need to contribute more cash.

They may need to accept a smaller loan.

They may also wonder whether the flat will be easy to sell when they are ready for their next move.

The home has not changed. But the financial equation has.

This is why HDB owners should not look only at what their flat is worth today. They should also consider who will realistically be able and willing to purchase it five or ten years from now.

Three Factors Matter When Planning an HDB Exit

Most homeowners focus almost entirely on price.

But a successful property exit depends on three connected factors.

1. Price

What price can similar units realistically achieve?

An asking price may look attractive, but it means little without sufficient demand from qualified buyers.

2. Timeline

How much time do you have to sell?

An owner with no deadline can wait for the right buyer. Someone who must complete a sale before purchasing the next home may have far less flexibility.

3. Buyer Pool

Who is most likely to buy the flat?

Will it appeal to young families, mature buyers, buyers prioritising space, or those who can contribute more cash?

The narrower the buyer pool, the more important pricing, positioning and timing become.

This Matters More for Certain Types of HDB Flats

The issue is especially relevant for owners of older:

Executive apartments

Executive maisonettes

Five-room flats

Flats in mature estates

Large units were purchased many years ago for their space

Many of these homes remain highly desirable. Some have layouts that are difficult to replicate in newer developments.

However, their future performance may depend on whether the advantages of size and location are sufficient to offset the shorter lease.

Instead of asking only:

“Can my HDB still be sold?”

A more useful question is:

“Who is likely to buy my HDB when I eventually need to sell?”

The difference between 70, 60 and 50 years of remaining lease is not merely a number on paper. Each stage can change the age, financial position and motivations of the buyers who are comfortable entering the market.

Do Not Wait Until Selling Becomes Urgent

Many homeowners intend to hold their flat until they genuinely need to move.

The problem is that the moment you urgently need to sell may not be the moment when you have the greatest negotiating power.

The eventual reason for moving may have little to do with investment:

Retirement

Health considerations

Children moving out

Estate planning

A need to right-size

A desire to unlock cash

Moving closer to family

When that happens, having a broad pool of buyers gives you flexibility.

A narrow buyer pool gives the market more control over your timeline and selling price.

Good property planning therefore begins before there is urgency. It gives you time to assess the numbers, understand your alternatives and decide whether holding, selling or right-sizing creates the best outcome.

Selling Is Not Automatically the Right Answer

Not every owner of an ageing HDB flat should sell.

Some flats continue to enjoy strong demand because of their location, size, layout or proximity to schools and amenities. Some owners may also have no better use for the capital and genuinely prefer to remain in their current home.

In these situations, holding can still be the right decision.

But holding should be an informed decision—not something done simply because the flat is comfortable and fully paid.

Before deciding, consider:

How many years of lease will remain when you are likely to sell?

Who will your future buyers be?

Will those buyers be able to use sufficient CPF and financing?

What newer alternatives will your flat be competing against?

How long might you need to secure the right offer?

What would you purchase after selling?

Would the next property improve your lifestyle, retirement security or capital position?

Selling without a better plan is unnecessary.

Holding without understanding the future risks is equally unwise.

Subscribe to our newsletter if you enjoy insights like this.

Think of It as Capital Repositioning

For many families, their HDB flat is one of their largest assets.

The decision to sell should therefore not be driven by fear of lease decay or excitement about upgrading. It should be treated as a capital-repositioning decision.

You are moving capital from one asset into another.

The new home should ideally improve at least one of these areas:

Your family’s lifestyle

Your retirement position

Your property’s future liquidity

Your potential for capital appreciation

Your ability to unlock or preserve cash

Otherwise, moving for the sake of moving may create more cost than value.

Unsure Whether to Hold or Sell Your HDB?

We help HDB owners assess where their property sits in its life cycle, how the remaining lease may affect the future buyer pool, and whether holding, upgrading or right-sizing makes the most financial sense.

There is no obligation to sell.

The objective is simply to understand your options clearly—so that your eventual decision is based on strategy rather than assumption.

Comments