London Stock Exchange Group: FY2025 and Q1 2026 performance

- Ben Tan

- Apr 30

- 6 min read

When I look at the London Stock Exchange Group, or LSEG, I do not see it as just a stock exchange.

To me, LSEG is more like a financial data and market infrastructure business. It provides the data, analytics, indices, trading infrastructure, risk tools, and workflow solutions that financial institutions rely on every day.

You may want to read my detailed analysis of the London Stock Exchange Group.

So when we analyse LSEG, the key question is not just whether revenue grew.

The better question is this:

Is LSEG becoming more important to its customers over time?

Based on FY2025 and Q1 2026, I think the answer is still yes — but there are a few things investors need to watch.

Before we go further, a quick disclaimer: I am a shareholder of the London Stock Exchange Group, so this is not investment advice. This is how I think through the business as an investor.

London Stock Exchange Group FY2025 performance: Still growing, but ASV needs monitoring

LSEG delivered a solid FY2025.

The business grew. Earnings improved. Cash generation remained strong. But the one metric I would watch closely is ASV, or Annualised Subscription Value.

ASV grew 5.9% in FY2025.

For a company like LSEG, ASV matters because it tells us whether its recurring subscription business is still expanding. This includes areas like data, analytics, indices, risk intelligence, and workflow tools.

A 5.9% growth rate is not bad. It still shows growth. But for a premium financial data business, I would ideally like to see this number comfortably above 6%.

This does not break the investment case, but it is something I would continue to monitor. If ASV keeps slowing, investors may start questioning whether LSEG’s data business is facing pricing pressure or maturity.

The good news is that the rest of the business performed well.

FY2025 organic income growth was 7.1%. This growth was broad-based across the group, with contributions from Data & Analytics, FTSE Russell, Risk Intelligence, and Markets.

That is important because LSEG is not relying on just one growth engine.

Its subscription businesses provide recurring revenue, while its Markets business can benefit when trading activity and market volatility are higher.

The earnings trend was also strong.

Adjusted EPS grew 15.7% to 420.6p. That means earnings grew faster than revenue, which is what you want to see from a high-quality business.

Cash generation was also strong.

LSEG generated around £2.4 billion of equity-free cash flow in FY2025, even after spending £919 million in capex.

This matters because profits can sometimes be accounting numbers. Cash flow is harder to fake. And when a company can generate strong free cash flow, it gives management more options, such as reinvesting in the business, reducing debt, paying dividends, or buying back shares.

So overall, FY2025 was a good year.

My simple summary would be:

LSEG is still growing, still profitable, and still generating strong cash. But ASV growth is the metric I would keep an eye on.

Subscribe to our newsletter if you enjoy insights like this.

Q1 2026 performance: Momentum improved

If FY2025 was solid, then Q1 2026 was more encouraging.

LSEG reported 9.8% growth in total income excluding recoveries for Q1 2026. This was a stronger growth rate than FY2025 and also strong enough for management to guide 2026 revenue growth towards the upper half of its 6.5% to 7.5% range.

By division, the growth was quite healthy:

Data & Analytics | +5.1% |

FTSE Russell | +8.8% |

Risk Intelligence | +10.5% |

Markets | +15.5% |

The standout was clearly Markets, which grew 15.5%.

This was helped by strong trading volumes and Tradeweb. But we need to be careful here. Markets can be more cyclical because trading activity may not stay elevated forever.

The more encouraging part, in my opinion, was the subscription side.

LSEG said its subscription businesses grew 6.3% in Q1 2026. That is better than the 5.9% ASV growth in FY2025.

This suggests that subscription momentum may be improving.

Again, one quarter does not make a trend. But it is a positive sign.

LSEG also continued to return cash to shareholders. In Q1 2026, it returned £1.1 billion through buybacks and remained on track to return £3 billion by February 2027.

So my take on Q1 2026 is this:

The business entered 2026 with better momentum. Growth accelerated, subscription growth improved, and capital returns remained strong.

Subscribe to our newsletter if you enjoy insights like this.

My top three concerns as a London Stock Exchange Group shareholder

Even though LSEG is a high-quality business, it is not without concerns.

These are the three I would watch.

Concern 1: ASV Growth Is Not Strong Enough Yet

The first concern is ASV growth.

As mentioned earlier, ASV grew 5.9% in FY2025. That is still growth, but for a premium data and analytics company, I would prefer something stronger.

Why does this matter?

Because LSEG’s valuation depends heavily on the quality and durability of its recurring revenue.

If ASV growth slows further, investors may start asking:

Is the business becoming too mature?

Are customers pushing back on pricing?

Are competitors or AI tools affecting demand?

The company is trying to address this by improving product adoption, expanding data delivery channels, and integrating its data into more customer workflows.

The early Q1 2026 number was encouraging, with subscription businesses growing 6.3%.

So I would say this concern is not fully resolved, but the direction is better.

Concern 2: AI Could Disrupt How Customers Use Financial Data

The second concern is AI.

This is probably one of the biggest questions investors have today.

Will AI make LSEG more valuable?

Or will AI reduce the need for traditional data terminals and expensive financial data products?

My view is that AI is both a risk and an opportunity.

The risk is that customers may not want to use financial data the old way anymore. Instead of logging into traditional screens or terminals, they may want to access insights through AI assistants, APIs, cloud platforms, or internal tools.

If that happens, LSEG’s interface may become less important.

But LSEG’s data may become even more important.

That is the key distinction.

LSEG is not just selling information. It is selling trusted, licensed, structured, financial-grade data. In finance, this matters a lot.

You cannot just rely on random AI answers when you are making investment, trading, compliance, or risk decisions. You need accurate, auditable, high-quality data.

This is where LSEG can still win.

The company is already moving in this direction through AI-related partnerships with companies such as OpenAI, Anthropic, Microsoft, Databricks, Snowflake, and Rogo.

It is also rolling out Workspace AI and building ways for customers to connect to LSEG data through AI workflows.

So my view is this:

AI is a threat if LSEG remains just a traditional interface. But AI is a complement if LSEG becomes the trusted data layer behind financial AI tools.

For now, the company seems to be moving in the right direction.

Concern 3: Margin, Portfolio, and Shareholder Pressure

The third concern is around execution and shareholder pressure.

LSEG became a much larger and more complex company after acquiring Refinitiv.

So naturally, investors want to know:

Can management simplify the business?

Can margins improve?

Can the company generate strong cash flow?

Can shareholders benefit from the acquisition?

There has also been pressure from activist investor Elliott Management, which reportedly pushed for better margins, more portfolio discipline, and stronger capital returns.

To be fair, LSEG has responded quite well.

FY2025 adjusted EPS grew 15.7%. Equity-free cash flow reached around £2.4 billion. The company also increased its dividend and announced a large £3 billion buyback programme.

This shows that the business is not just growing revenue. It is also converting that growth into earnings and cash.

Want a concise version of Charlie Munger’s 25 human misjudgements? Download here!

Final view

Overall, I think LSEG remains a high-quality financial infrastructure and data business.

FY2025 showed that the business is still growing, earnings are compounding faster than revenue, and cash generation is strong.

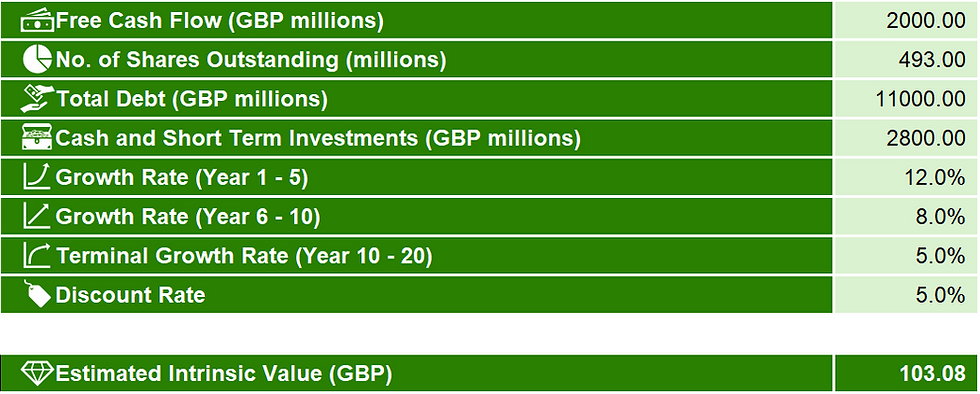

Q1 2026 was even more encouraging because growth accelerated and subscription momentum improved. I have also updated my intrinsic value for LSEG to approximately £103.00

But this is not a stock where I would just look at headline revenue growth and move on.

For LSEG, I would monitor three things closely:

First, can ASV and subscription growth stay above 6%?

Second, can AI deepen customer usage instead of pressuring pricing?

Third, can the company continue to expand margins and generate strong free cash flow after the Refinitiv integration benefits mature?

Let me know what you think about the London Stock Exchange Group.

Subscribe to our newsletter if you enjoy insights like this.

Comments